Algorithmic trading automates rule-based strategies to execute faster, remove emotion, and scale trading with backtesting and risk controls.

Algorithmic trading uses computer programs to execute trades based on pre-determined rules such as price, time, volume, and risk limits. It is designed to improve consistency, speed, and execution quality while reducing emotional decision-making, which is why it is widely used by both institutional and retail traders. In practice, algorithmic systems can monitor multiple markets simultaneously, react to data in real time, and keep operating around the clock when the underlying market is open.

Here’s what you’ll learn:

- How algorithmic trading works: automation, rule-based logic, data analysis, and efficient execution.

- Popular strategies: trend-following, mean reversion, arbitrage, and market-making.

- Tools and technologies: programming languages like Python, platforms like TradingView, and AI-assisted trading development with LuxAlgo Quant.

- Benefits vs. risks: speed and precision vs. technical failures, model drift, and execution risk.

- Steps to get started: define a strategy, backtest it, optimize it, deploy it carefully, and monitor performance.

Algorithmic trading gives traders a structured way to automate ideas, validate them on historical data, and improve workflow efficiency while managing risk through proper testing, monitoring, and disciplined execution.

What Is Algorithmic Trading? A Beginner’s Guide to Automated Strategies

What Is Algorithmic Trading?

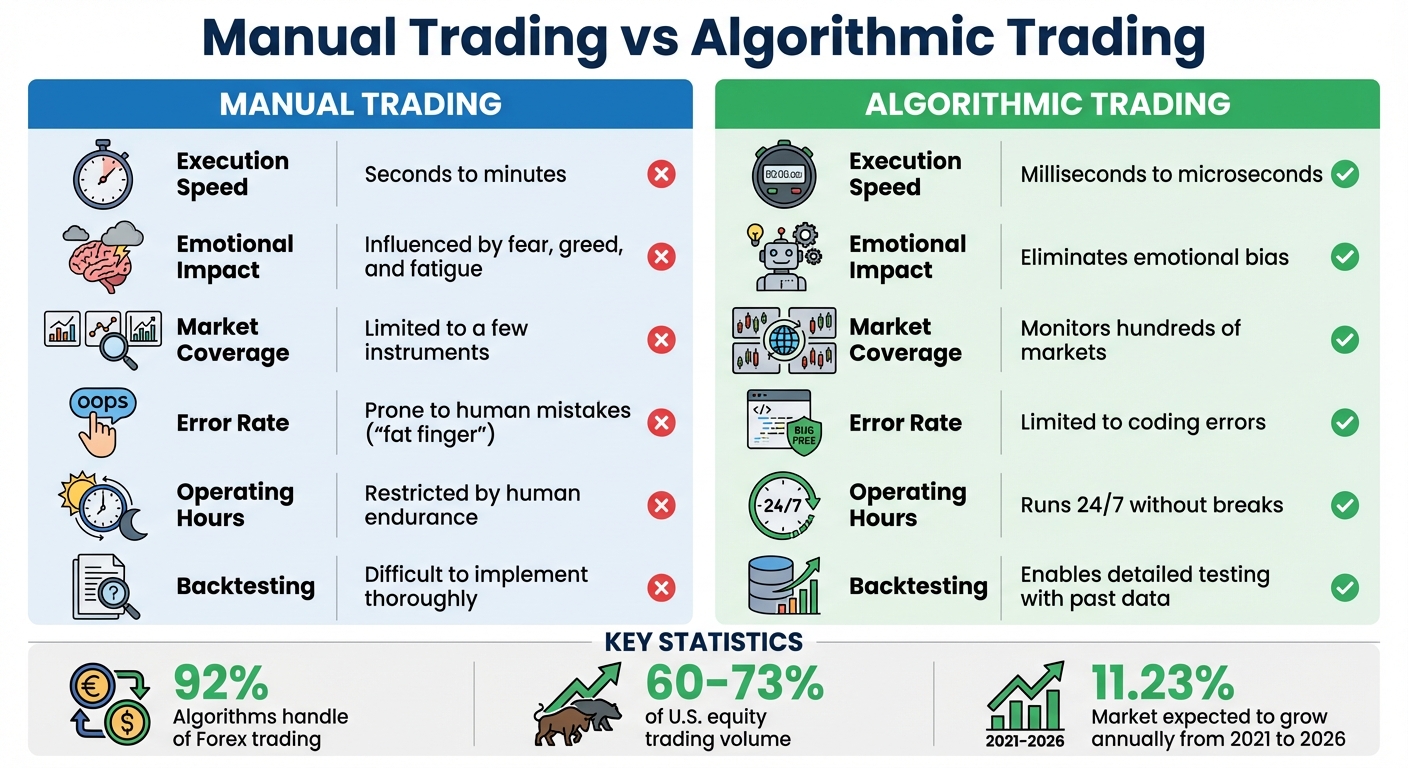

Manual vs Algorithmic Trading: Key Differences Comparison

Algorithmic trading uses automated, pre-set instructions to execute trades based on factors such as time, price, volume, volatility, or indicator signals. Instead of manually clicking “buy” or “sell,” traders rely on coded rules to monitor markets, identify opportunities, and place orders automatically. This rule-based approach is one reason algorithmic trading has become so important across modern financial markets, as described in the SEC’s report on algorithmic trading in U.S. capital markets.

The appeal of algorithmic trading lies in its speed, scale, and consistency. Algorithms can process large amounts of market data and react in milliseconds, far faster than any human trader. They can also monitor many symbols at once, something that is difficult to do manually. In contrast, discretionary trading can be affected by fear, greed, fatigue, hesitation, and basic order-entry mistakes.

Algorithmic trading has also become more accessible. What once required custom infrastructure and in-house quant teams can now be explored by independent traders using platforms such as TradingView, broker APIs, and specialized development environments. For traders who want to convert an idea into TradingView logic more quickly, LuxAlgo Quant can help generate, validate, and refine Pine Script® indicators and strategies from plain-language prompts or chart references.

Next, let’s explore the principles that make algorithmic trading effective in real market conditions.

Core Principles of Algorithmic Trading

Algorithmic trading operates on four key principles:

- Automation: Once a strategy is configured, computers can handle signal detection, order generation, and execution without constant human intervention.

- Rule-Based Logic: Algorithms follow explicit “if-then” conditions. For example: “If the 50-day moving average crosses above the 200-day moving average, open a long position.” This keeps decisions consistent and testable.

- Data-Driven Decisions: Algorithms evaluate real-time and historical data to detect patterns, changes in volatility, or execution opportunities that may be difficult to track manually.

- Efficient Execution: Algorithms can break larger orders into smaller pieces using methods such as VWAP or TWAP to reduce market impact and improve fill quality.

At a high level, successful algorithmic trading is less about finding a “magic” indicator and more about defining repeatable logic, validating it carefully, and executing it with discipline. That is also why traders increasingly pair development with robust backtesting and validation workflows before going live.

To make these principles work in practice, algorithmic trading systems rely on several core components.

Key Components of Algorithmic Trading Systems

Turning these principles into action requires a well-designed system with four main components:

Data Inputs:

The foundation of any algorithmic system is a reliable stream of market data, including price updates, OHLC bars, volume, and, in some cases, order book depth. More advanced workflows may also use macro releases, sentiment data, or other alternative datasets, but the quality and cleanliness of the data feed remain critical.

The Algorithm:

This is the system’s decision engine, often written in languages such as Python, MQL5, C#, or Pine Script®. It defines entry rules, exits, position sizing, filters, and risk controls. If you are building specifically for TradingView, Quant is especially relevant because it is purpose-built for Pine Script generation, debugging, and validation rather than being a general-purpose chatbot.

Execution Mechanism:

This component connects the algorithm to a broker or exchange, usually through an API, and handles the actual placement and management of orders. For faster strategies, infrastructure quality matters because delays, slippage, and order-routing issues can materially change outcomes.

Monitoring and Risk Management:

A trading system needs constant supervision even when entries and exits are automated. That includes monitoring drawdowns, checking trade logs, enforcing stop-loss rules, limiting exposure, and using a “kill switch” that can stop the strategy if something abnormal happens.

| Feature | Manual Trading | Algorithmic Trading |

|---|---|---|

| Execution Speed | Seconds to minutes | Milliseconds to microseconds |

| Emotional Impact | Influenced by fear, greed, and fatigue | Designed to reduce emotional bias |

| Market Coverage | Limited to a few instruments | Can monitor many markets simultaneously |

| Error Rate | Prone to manual input mistakes | More dependent on code and data quality |

| Operating Hours | Restricted by human availability | Can run continuously when supported |

| Backtesting | Harder to perform thoroughly | Enables detailed testing with historical data |

This comparison highlights the trade-off clearly: manual trading offers flexibility and intuition, while algorithmic trading offers structure, repeatability, and scalability. The challenge is making sure the automated system is robust enough to handle real-world market behavior.

How Algorithmic Trading Works

Understanding the mechanics of algorithmic trading makes the technology behind automated markets much less intimidating. In practical terms, the process has two main phases: developing and testing the strategy and executing and automating the trades. Both require precision, good data, and realistic expectations.

Developing and Testing Strategies

Creating an effective strategy starts with defining clear logic. That might mean buying when one moving average crosses another, exiting when volatility expands beyond a threshold, or avoiding trades during major economic releases. The key is that the logic must be specific enough to code, test, and review.

Once the rules are defined, the next step is to turn them into code. Many traders use Python or platform-native languages, while TradingView users often build in Pine Script®. If you want to shorten the path from concept to implementation, LuxAlgo Quant can help turn strategy ideas into working Pine Script, fix bugs, and iterate on custom indicator or strategy logic much faster than starting from scratch.

After coding comes backtesting, where the strategy is run against historical data to evaluate performance. This step helps uncover strengths and weaknesses, but it should be done carefully. Backtests can look impressive for the wrong reasons if the model has been overfit to the past. That is why out-of-sample testing, walk-forward analysis, and robustness checks matter so much.

Paper trading comes next. In a paper environment, the algorithm sees live market conditions without risking real capital. This is one of the best ways to uncover real-world execution issues such as missed fills, latency, slippage, and order handling differences that may not show up in a clean historical simulation.

| Aspect | Paper Trading | Live Trading |

|---|---|---|

| Execution Speed | Often assumes ideal fills | Affected by latency and slippage |

| Market Impact | None | Orders can affect fill quality |

| Emotional Factor | Low stress | Higher emotional pressure |

| Order Fills | Usually optimistic | Can face gaps, partial fills, or rejection |

The final pre-live step is ongoing monitoring and maintenance. Markets evolve, and strategies can lose effectiveness over time. Traders should regularly review metrics such as drawdown, win rate, profit factor, and risk-adjusted return rather than relying only on top-line profit. A kill switch and daily risk limits are not optional extras; they are part of responsible system design.

Once the strategy is validated, the focus shifts from design to execution.

Order Execution and Automation

When a validated strategy receives a signal, the algorithm converts that signal into an order and routes it to a broker or exchange. The process can happen very quickly, but speed alone is not enough. Reliable execution depends on stable infrastructure, accurate order handling, and risk checks that run before the order is sent.

Here’s how the execution flow usually works:

| Step | Action | Description |

|---|---|---|

| 1. Signal | Detection | Example: a moving-average crossover or breakout condition is triggered |

| 2. Order | Placement | The system sends a market, limit, or stop order to the broker |

| 3. Risk Limit | Validation | Position size, stop-loss, and exposure caps are checked |

| 4. Execution | Routing | Order routing seeks better fills and lower execution costs |

| 5. Logging | Recording | Trade details are stored for analysis, compliance, and review |

The choice of order type matters. Market orders prioritize immediate execution, while limit orders prioritize price control. Stop-loss orders help cap downside risk, and take-profit orders automate exits at target levels. More sophisticated workflows can use smart order routing, participation rules, or execution benchmarks depending on the venue and asset class.

Infrastructure also plays a major role. A VPS or cloud deployment can improve uptime and reduce connectivity issues, while more latency-sensitive participants may use co-location or premium data routing. Even then, the objective should not be to “win the speed race” blindly; it should be to make sure the strategy’s actual edge survives realistic execution conditions.

“Electronic trading and algorithmic trading are both widespread and integral to the operation of our capital markets.” — U.S. Securities and Exchange Commission

Common Algorithmic Trading Strategies

Algorithmic trading relies on clearly defined rules, but the rules themselves can vary widely. Some strategies try to ride strong trends, while others attempt to capture reversions, pricing gaps, or the spread between bid and ask prices. Understanding the environment each strategy is designed for is just as important as understanding the strategy itself.

Trend-Following Strategies

Trend-following strategies aim to capture sustained price moves by aligning with the dominant market direction. One familiar example is the “Golden Cross,” where a shorter moving average crosses above a longer one. Trend systems may also use momentum filters, breakout levels, ATR-based stops, or confirmation from volume and structure.

Indicators such as the Relative Strength Index (RSI) and Average True Range (ATR) can help measure momentum and volatility. These strategies tend to perform best in strongly directional environments, but they can struggle when the market chops sideways and repeatedly triggers false breakouts.

Because trend-following is naturally rule-based, it is also a good fit for AI-assisted development. Traders who want to prototype moving-average systems, momentum filters, or breakout logic on TradingView can use Quant to create Pine Script strategies faster and then refine the logic after reviewing backtest results.

Mean Reversion Strategies

Mean reversion strategies are based on the idea that prices often oscillate around an average value and may eventually return toward it after becoming stretched. Common tools include Bollinger Bands, standard deviation channels, Z-scores, and momentum exhaustion signals.

These strategies often work better in range-bound conditions than in strong trends. The main risk is obvious but important: markets can stay extended for much longer than expected, and a system that keeps fading strength without a solid risk framework can accumulate losses quickly.

Arbitrage Strategies

Arbitrage strategies attempt to profit from pricing differences between related instruments, exchanges, or structures. Examples include spatial arbitrage across venues, triangular arbitrage in currencies, and statistical arbitrage across correlated assets.

These opportunities are usually short-lived, which means execution quality and transaction costs are critical. Many apparent arbitrage setups disappear once fees, spread, and latency are accounted for, so traders should be careful not to assume that every theoretical pricing gap is practically tradeable.

Market-Making Strategies

Market-making algorithms place buy and sell quotes around the current market price and try to earn the bid-ask spread. In liquid markets, that can create many small opportunities, but it also introduces inventory risk when the market suddenly trends hard in one direction.

These strategies are usually more infrastructure-sensitive than beginner trend systems. They require strong execution, inventory controls, and careful quote management, especially during fast markets or liquidity shocks.

| Strategy Type | Ideal Market Condition | Primary Goal | Key Risk |

|---|---|---|---|

| Trend-Following | Trending / volatile | Capture sustained directional moves | False breakouts and reversals |

| Mean Reversion | Stable / ranging | Profit from price returning to an average | Persistent trends |

| Arbitrage | Inefficient / fragmented | Exploit temporary price discrepancies | Latency and transaction costs |

| Market-Making | High liquidity | Earn the bid-ask spread | Inventory risk |

Tools and Technologies for Algorithmic Trading

Building a robust algorithmic trading workflow typically means combining programming tools, charting platforms, market data, backtesting frameworks, and execution infrastructure. The exact stack depends on the trader’s market, platform, and strategy horizon, but the broad categories are similar across most workflows.

Programming and Charting Platforms

Python remains one of the most popular languages for algorithmic trading because of its rich ecosystem. Pandas and NumPy are widely used for working with market data, while TA-Lib helps calculate common technical indicators. Frameworks such as Backtrader and Vectorbt are often used for historical strategy testing, while Scikit-learn and TensorFlow support machine-learning workflows.

On the charting side, TradingView remains a popular environment for visualization, alerting, and developing rule-based logic with Pine Script®. For traders working specifically in that ecosystem, LuxAlgo Quant is particularly useful because it is specialized for Pine Script indicator and strategy creation, debugging, and iterative refinement.

LuxAlgo’s Specialized Toolkits

LuxAlgo provides structured ways to apply technical analysis on TradingView by turning complex concepts into more systematic workflows. Its three primary TradingView toolkits are:

- Price Action Concepts®: Automates price-action analysis such as market structure, order blocks, and fair value gaps, helping traders reduce subjectivity.

- Signals & Overlays®: Focuses on trend, overlays, signals, and alert-ready analysis designed for live chart decision-making.

- Oscillator Matrix®: Tracks momentum and money-flow behavior to help identify divergences, trend conditions, and potential exhaustion.

These toolkits are complemented by dedicated Screeners and Backtesters, which help traders move from chart observation into strategy evaluation and filtering. If your workflow is more code-driven, the bridge between discretionary chart analysis and custom automation is often Quant, since it can turn TradingView ideas into executable Pine Script strategies more directly.

For traders who want to learn the platform structure in more detail, the LuxAlgo introduction and TradingView setup guide are useful starting points.

AI-Powered Features

AI is increasingly becoming part of the algorithmic trading workflow, especially in research, coding, and validation. Instead of manually building every script line by line, traders can now speed up development with systems designed for market-specific tasks.

LuxAlgo Quant is an AI coding agent specialized in generating and validating Pine Script® indicators and strategies for TradingView. It can help convert plain-language strategy ideas into code, debug Pine Script, refine custom logic, and even support chart- or image-to-code workflows. That makes it especially relevant for traders who want to move from concept to deployable TradingView logic faster.

LuxAlgo’s AI Backtesting Assistant complements that workflow by helping traders search, test, and compare strategy ideas more efficiently. Instead of manually rebuilding every possible variation, traders can use the platform to find strategies aligned with certain conditions, performance thresholds, or toolkit logic before replicating them on TradingView.

| Python Library Category | Examples | Purpose |

|---|---|---|

| Data Fetching | yfinance, Alpha Vantage | Accessing historical and live market data |

| Data Manipulation | Pandas, NumPy | Managing datasets and calculations |

| Technical Analysis | TA-Lib | Computing indicators like RSI, MACD, and Bollinger Bands |

| Backtesting | Backtrader, Vectorbt | Testing strategies on historical data |

| Machine Learning | Scikit-learn, TensorFlow | Developing predictive and classification models |

Benefits and Challenges of Algorithmic Trading

Benefits of Algorithmic Trading

Algorithmic trading offers several advantages that make it attractive in modern markets. The most obvious is speed: algorithms can react to signals much faster than manual traders. Another key benefit is consistency. Once rules are defined, the system applies them the same way every time instead of changing behavior because of stress or hesitation.

Another strength is precision. Algorithms can enforce exact position sizes, stop-loss distances, time filters, and execution rules. They can also watch many instruments at once and remain active across sessions, which is useful for global markets such as forex and crypto. Finally, they allow for systematic backtesting, helping traders evaluate a strategy before deploying real capital.

Challenges and Risks

Despite those benefits, algorithmic trading introduces serious risks. The first is technical complexity. Code bugs, poor data quality, unstable connectivity, or broker-side execution issues can all damage performance quickly. Even a strategy with a genuine edge can fail if the implementation is weak.

Over-optimization is another major pitfall. A model can look excellent in a backtest because it has been tuned too closely to historical noise rather than repeatable behavior. This is why traders should use out-of-sample testing, forward testing, and robust validation rather than trusting a single optimized result.

There is also regulatory and structural risk. Market abuse practices such as spoofing are actively enforced against, and market stress events can produce sudden liquidity gaps or trading halts. For example, U.S. markets use market-wide circuit breakers to temporarily pause trading during severe declines.

Finally, every strategy faces regime risk. A trend system can underperform badly in sideways markets, while mean-reversion systems can fail during persistent directional moves. Automation reduces emotional error, but it does not eliminate uncertainty or market change.

“Now it’s an arms race. Everyone is building more sophisticated algorithms, and the more competition exists, the smaller the profits.” — Andrew Lo, Director of the Laboratory for Financial Engineering, MIT

Pros and Cons Comparison Table

| Benefits | Challenges & Risks |

|---|---|

| Speed & Precision: Executes rules rapidly and consistently | Technical Failures: Vulnerable to bugs, data issues, or outages |

| Reduced Emotional Bias: Follows predefined logic | Over-optimization: May fail outside test conditions |

| 24/7 Monitoring Potential: Useful for global markets | Infrastructure Costs: Better execution often needs better systems |

| Scalability: Can monitor multiple markets at once | Regulatory Scrutiny: Improper behavior can create legal risk |

| Backtestability: Allows structured evaluation of ideas | Market Shocks: Sudden volatility can break assumptions |

To reduce these risks, traders should build risk controls directly into their system. That includes stop-losses, maximum position sizes, exposure caps, trading session filters, kill switches, and post-trade monitoring. Diversifying across strategies or market conditions can also reduce dependence on any single edge.

Getting Started with Algorithmic Trading Using LuxAlgo

Define Your Strategy and Goals

To get started, define the market you want to trade, your time horizon, and the type of edge you are trying to capture. That could be trend-following in forex, mean reversion in equities, or breakout logic in crypto. Keep the first version simple enough to test clearly rather than trying to solve every market condition at once.

It also helps to set practical expectations around return, drawdown, and position risk. Clear risk limits make it easier to evaluate whether a strategy is actually suitable for your account size and trading style. In most cases, it is better to start with a strategy that is understandable and robust than one that looks impressive only because it has been over-optimized.

LuxAlgo’s AI Backtesting Assistant can help speed up the research stage by surfacing strategy ideas and backtested workflows that fit particular conditions. If you want to create or customize your own TradingView logic, Quant can translate your concept into Pine Script and help iterate on the logic more efficiently.

Once your rules and objectives are clear, the next step is choosing the right tooling.

Use LuxAlgo’s Free and Premium Tools

LuxAlgo’s Library gives traders free access to a broad collection of indicators across multiple charting platforms. That makes it a practical starting point for exploring structured workflows before moving into more advanced automation.

For traders who want deeper TradingView functionality, LuxAlgo also provides exclusive tools including Toolkits, Screeners, Backtesters, Quant, and the AI Backtesting Assistant. The current plan structure is straightforward: the Free plan is $0 with lifetime access, Premium is $39.99/month with advanced TradingView capabilities and higher Quant usage limits, and Ultimate is $59.99/month with access to AI Backtesting plus higher-tier access across LuxAlgo features.

That structure lets traders choose a workflow that matches how they actually operate. Some users mainly want better chart analysis and alerting on TradingView, while others want AI-assisted Pine Script creation, debugging, and backtesting support. If your workflow centers on coding indicators or strategies, Quant is often the most relevant place to start.

Backtest and Optimize Your Strategies

Once you have a strategy idea, backtesting is the next essential step. With AI Backtesting, traders can explore and compare strategy behavior across supported markets and timeframes using natural-language requests. That can significantly shorten the time spent manually filtering for ideas that meet certain requirements.

Optimization should be used carefully. The goal is not to force a strategy to look perfect on historical data, but to find settings that remain sensible across multiple periods and conditions. Walk-forward analysis, out-of-sample testing, and simpler rule sets often provide more durable results than aggressively tuned parameters.

For custom TradingView builds, Quant can also help here by making it easier to modify Pine Script rules, test different signal conditions, and debug logic without having to rewrite entire sections of code manually.

Once a strategy is sufficiently tested, it can move into live monitoring.

Deploy and Monitor on TradingView

After backtesting, traders can deploy the workflow on TradingView for chart-based monitoring, alerting, and ongoing refinement. LuxAlgo’s setup documentation explains how to connect accounts and access exclusive TradingView functionality.

From there, alerts can be configured to notify you when conditions are met, and automated routing can be handled externally where supported. Monitoring should remain active even after launch: review fills, compare live performance to test assumptions, and confirm that risk controls are still working as intended.

A practical workflow for many traders is to research with AI Backtesting, convert custom logic into Pine Script with Quant, deploy the script on TradingView, and then use alerts and review cycles to keep the system aligned with current market conditions.

Conclusion

Algorithmic trading has reshaped how traders approach the markets by combining structure, speed, and repeatable execution. Whether you are building a simple rules-based system or a more advanced TradingView workflow, the fundamentals remain the same: define the rules clearly, test them honestly, manage risk carefully, and monitor performance continuously.

LuxAlgo helps bridge the gap between theory and implementation. Traders can use Quant to build and validate Pine Script indicators and strategies, while the AI Backtesting Assistant helps surface and evaluate strategy ideas more efficiently. On top of that, products such as Price Action Concepts, Signals & Overlays, and Oscillator Matrix make it easier to turn market observations into structured decision-making.

The key is to treat automation as a process, not a shortcut. Good algorithmic trading comes from combining sound ideas, realistic validation, disciplined deployment, and continuous review. Whether you begin with free indicators, custom Pine Script development, or AI-assisted strategy research, the most important step is starting with a workflow you can understand and improve over time.

If you are ready to move from chart ideas into more systematic execution, focus first on a single market, a clear rule set, and a robust testing process. From there, you can expand carefully with better tools, better data, and better automation.

FAQs

Do I need to know coding to start algorithmic trading?

You do not need to be a programmer to begin exploring algorithmic trading. Many platforms provide pre-built indicators, configurable alerts, and visual strategy tools that let traders test structured ideas without writing every line of code. That said, learning the basics of how rules, data, and execution work will still make you a better user of those tools.

If you specifically want to build on TradingView, tools like LuxAlgo Quant can reduce the coding barrier by helping translate plain-language ideas into Pine Script strategies and indicators, which is useful for traders who want customization without starting from a blank editor.

How can I tell if my backtest is overfitted?

Overfitting happens when a strategy is tuned too closely to past data and ends up modeling noise instead of repeatable market behavior. The result is usually a backtest that looks excellent historically but performs poorly in live or forward conditions.

Signs of Overfitting

- Excellent historical performance that quickly breaks down in paper or live trading

- Extreme sensitivity to small parameter changes

- Too many rules or filters compared with the simplicity of the market idea

- Strong performance only in one narrow period or regime

How to Prevent It

- Use out-of-sample data so the strategy is tested on information it was not optimized on

- Apply walk-forward analysis to evaluate stability over time

- Prefer simpler models unless added complexity is clearly justified

- Forward test in a paper environment before risking real capital

By watching for these warning signs and using stronger validation methods, traders can improve the odds that a strategy holds up outside the backtest window.

What risk controls should every trading algorithm include?

Every trading algorithm should include strong risk controls to reduce the damage from bad signals, technical failures, or sudden market shocks. At a minimum, that usually means position limits, stop-loss logic, maximum daily loss limits, and an emergency kill switch that can halt trading if something abnormal happens.

It is also important to include sensible position sizing, limits on correlated exposure, and monitoring for execution anomalies such as repeated rejections or unusually high slippage. Risk controls should not sit outside the workflow as an afterthought; they should be embedded directly into the design of the strategy.

References

LuxAlgo Resources

- LuxAlgo

- LuxAlgo Quant

- Quant Introduction

- Quant Features

- AI Backtesting Assistant

- What Is LuxAlgo?

- TradingView Setup Guide

- LuxAlgo Pricing

- LuxAlgo Library

- Stress Testing for Trading Strategies

- The Key to Understanding RSI

- FVG Instantaneous Mitigation Signals

- LuxAlgo Price Action Concepts