Explore the regulatory gray area of retail prop firms, highlighting risks for traders, key due diligence steps, and the importance of informed choices.

Retail proprietary trading firms (prop firms) offer traders access to capital in exchange for passing evaluation tests and sharing profits. However, these firms often operate in a regulatory gray area, leaving traders exposed to risks like sudden account closures, payout disputes, and data privacy concerns. Unlike regulated brokers, prop firms are not required to segregate funds, maintain financial reserves, or follow strict transparency rules.

How to Pass Prop Firm Challenges With Proven Trading Strategies

Passing a proprietary trading firm challenge isn’t about luck or over-leveraging—it’s about using strategies that are already aligned with real prop firm rules. Most traders fail challenges not because they can’t trade, but because their strategies weren’t designed to survive strict drawdown limits, daily loss caps, and consistency requirements.

At LuxAlgo, traders can access a dedicated prop firm strategies hub that makes it easy to find ready-to-use trading strategies specifically built for prop firm environments. These strategies are designed to:

- Have proven to work in the past across multiple market conditions

- Would have passed historical challenges based on real rule constraints

- Have a higher probability of passing current challenges without over-risking

Instead of guessing which approach might work, traders can explore strategies that have already been validated against the same risk rules used by many modern prop firms.

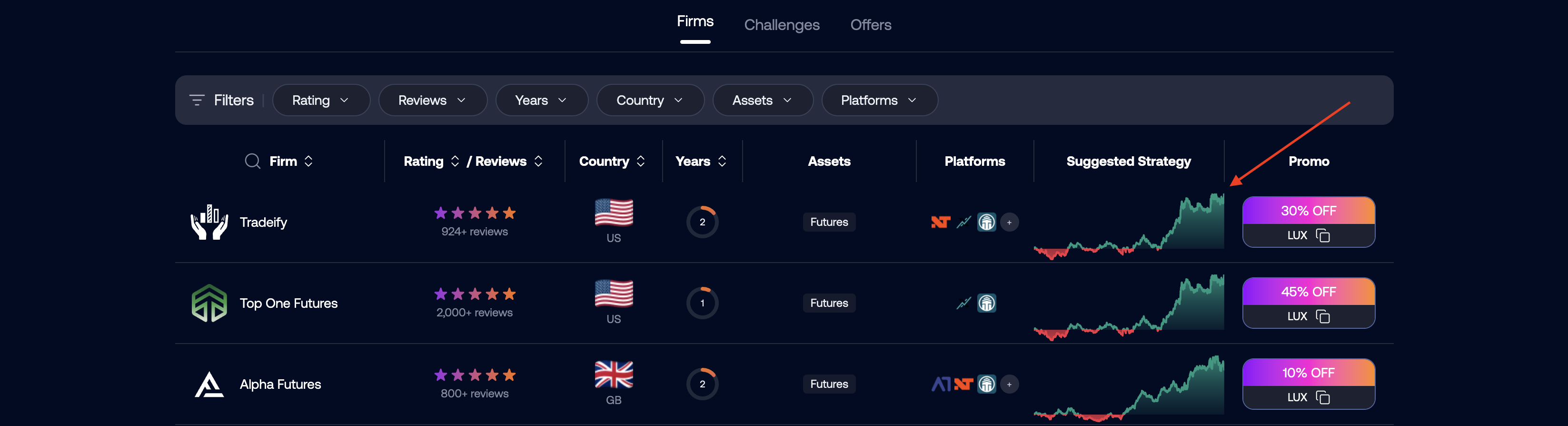

The LuxAlgo Prop Firms page acts as a central hub where traders can:

- Quickly access prop-firm-ready trading strategies

- Compare firms and rule structures in one place

- Apply strategies designed to respect drawdown and daily loss limits

- Receive high discounts on prop firm evaluations when available (as high as possible, when relevant)

For traders paying repeated evaluation fees, using strategies that are already aligned with prop firm requirements can reduce trial-and-error, prevent unnecessary resets, and improve the odds of reaching a funded stage more efficiently.

Suggested Strategies

These challenge-focused strategies are typically built around consistency and risk control—prioritizing compliance with daily loss limits, overall drawdown rules, and payout eligibility criteria, rather than aggressive exposure. To explore ready-to-use strategy options and quickly apply them to the prop firm environment you’re targeting, visit the LuxAlgo prop firm strategies page.

Key Points

- How Prop Firms Work: Traders pay fees to pass evaluations for access to firm capital, with profit-sharing models varying by firm.

- Regulation Gaps: Prop firms are largely unregulated in the U.S., avoiding oversight from agencies like the SEC, CFTC, and NFA.

- Risks for Traders: Unregulated firms can change rules, delay payouts, or shut down without recourse for traders.

- Due Diligence: Traders should verify a firm’s reputation, payout history, and legal documentation before joining.

- Future Changes: Regulatory updates may include stricter rules on marketing, transparency, and evaluation practices.

To protect yourself, research thoroughly, review all terms, and consider using advanced workflows to refine your trading strategies with AI Backtesting. While the industry’s regulatory landscape evolves, traders must remain vigilant and informed.

Are Prop Firms Even Legal?

Current U.S. Regulatory Framework

Navigating the regulatory world of retail prop firms in the U.S. can feel like stepping into a maze. With a mix of federal and state rules—and plenty of gaps in between—these companies often find themselves operating in a murky legal space. For traders, understanding how these rules apply (or don’t) is essential when evaluating a firm’s credibility and practices.

Federal Oversight: SEC, CFTC, and NFA

At the federal level, three key players oversee financial markets: the Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), and the National Futures Association (NFA). While traditional broker-dealers and futures commission merchants are subject to SEC and CFTC regulations, many retail prop firms structure themselves to sidestep these rules. For example, they often frame access as “evaluation + simulated funding,” charge participation fees, and position the relationship as a service contract rather than traditional brokerage activity.

The NFA, responsible for overseeing futures trading professionals, also doesn’t typically regulate retail prop firms unless a firm (or its counterparties) falls into categories that require registration. This creates a meaningful gap in routine oversight, especially compared with regulated intermediaries that face ongoing compliance obligations, examinations, and reporting standards.

State-Level Regulations and Blue Sky Laws

Even though federal agencies may not directly oversee retail prop firms, state-level regulations can still come into play. One key area of state oversight is through Blue Sky Laws, which aim to protect investors from fraud and deceptive practices. For a plain-English overview, see Blue Sky laws and their purpose. For additional context on how state securities laws coexist with federal rules, see NASAA’s overview of state securities acts.

These laws differ from state to state and can create a patchwork of requirements. In practice, this variability is one reason traders may see large differences in how firms describe eligibility, marketing, or consumer protections depending on the jurisdictions they serve.

The Unregulated Gray Area

The gaps in both federal and state oversight create a significant gray area where many retail prop firms operate. While these firms may still be subject to general consumer protection rules and fraud enforcement, they often avoid standardized requirements that apply to regulated intermediaries.

For example, without uniform rules, there’s no consistent requirement for financial reporting, capital reserves, or customer protection practices comparable to broker-dealer standards. Firms can adjust their policies—such as payout terms, eligibility rules, or fee structures—with limited restraint. When enforcement does happen, it’s often reactive, addressing problems only after traders have already been affected.

For traders, this uncertainty means taking on more responsibility. Without routine inspections or clear guidelines from regulatory bodies, traders must dig into a firm’s background themselves. Researching a firm’s business model, payout rules, and dispute process becomes critical. In this fragmented environment, the burden of due diligence falls squarely on the trader, not the system designed to protect them.

Risks of Using Unregulated Prop Firms

Unregulated prop firms exist in a murky space without the protections and oversight that come with regulation. This lack of oversight can expose traders to risks they wouldn’t typically face with regulated financial institutions. Without the safeguards provided by regulatory bodies, traders need to tread carefully and thoroughly investigate before investing their time or money. Let’s break down some of the specific risks involved.

Payout Disputes and Sudden Shutdowns

Unlike regulated brokers, unregulated prop firms don’t have to follow strict rules when it comes to payouts or maintaining financial reserves. This means they can change payout policies, eligibility conditions, or withdrawal timing with limited accountability. If the firm runs into financial trouble—or simply changes its internal policies—it could shut down or suspend payouts abruptly, leaving traders with little recourse.

It’s also worth recognizing how “low conversion to payout” can show up in real firm-reported data. For example, some firms publish annual performance statistics that show only a subset of participants advance to funded levels, and only a subset of funded traders receive payouts within a given year. Reviewing publicly posted stats (when available) can help set expectations before you pay evaluation fees Topstep’s published performance statistics.

Lack of Protection for Funds and Personal Data

Regulated brokers are required to separate customer assets from their own operating funds. For securities broker-dealers, this is closely tied to the SEC’s customer protection framework, and FINRA highlights the obligations associated with safeguarding customer funds and securities under the Customer Protection Rule (SEA Rule 15c3-3). Unregulated prop firms, however, may not follow comparable segregation practices, which can increase the risk that trader earnings or balances become entangled with the firm’s operational finances.

Beyond financial risks, these firms may also have weaker or less consistent data security measures. In regulated environments, AML and identity-related controls are part of the compliance landscape; for example, the SEC provides broker-dealer guidance and resources for building AML programs here. Many retail prop firms are not held to the same operational standards, so traders should treat data privacy and security policies as a key due diligence item.

Misleading Marketing and Ambiguous Terms

Unregulated firms frequently rely on aggressive marketing that downplays risks and glosses over important details. This can lead to unclear terms regarding payouts, account policies, or evaluation criteria. Fee structures can also be tricky, with hidden charges or ambiguous enforcement language that makes it harder for traders to fully understand what they’re signing up for.

Regulators have also increased scrutiny of promotional activity across the broader trading ecosystem—especially social-media-driven claims. For example, ASIC has publicly discussed enforcement actions and warnings aimed at “finfluencers” promoting high-risk financial products without proper licensing or disclosures ASIC release. While this is not “prop-firm-only,” it’s directly relevant to traders evaluating marketing claims in 2026.

Given these risks, it’s crucial for traders to do their homework. Carefully review all documentation, ask questions, and make sure you fully understand the terms and conditions before getting involved with any prop firm.

How Regulated Brokers Provide Protections

When comparing regulated brokers to unregulated proprietary (prop) firms, the differences in trader protections are striking. Regulated brokers in the United States operate under strict oversight, ensuring safeguards that are often missing in unregulated environments. These protections help traders make better-informed decisions about where to invest their capital and highlight the importance of understanding the role of regulation in trading.

Regulatory Requirements for Brokers

In the United States, regulated brokers are monitored by federal agencies like the Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), and the National Futures Association (NFA). These agencies enforce rigorous standards to ensure brokers operate transparently and responsibly.

Key requirements for regulated brokers include:

- Licensing: Brokers must obtain proper authorization to operate legally.

- Capital Reserves: They are required to maintain sufficient capital to ensure financial stability.

- Transparency: Regular audits and detailed financial reporting ensure brokers remain accountable.

Transparency rules are particularly important. Brokers must clearly disclose their fee structures, trading conditions, and business practices, giving traders a clearer understanding of what to expect. This level of oversight allows regulators to monitor brokers’ financial health and intervene if necessary, reducing risks for traders.

Protections for Traders: SIPC Insurance and Fund Segregation

These regulatory measures translate directly into protections for traders. One of the most critical safeguards is fund segregation, which helps ensure that customer assets are kept separate from the broker’s operational accounts. This means that even if a broker faces financial trouble, segregation rules are designed to reduce the risk that customer assets are used to cover the firm’s obligations.

Another layer of protection comes from SIPC insurance. The Securities Investor Protection Corporation (SIPC) provides coverage of up to $500,000 per customer account, including a $250,000 limit for cash claims. While SIPC doesn’t cover market losses, it can protect customers in specific scenarios involving broker-dealer failure and missing securities.

For traders in forex and futures markets, similar protections can apply through regulatory requirements that govern how customer money is held and reported. Additionally, many brokers go beyond baseline requirements by securing extra insurance coverage or implementing higher internal risk controls.

Regulated environments also provide structured dispute resolution options. For example, the NFA offers an arbitration program, giving traders a formal channel to resolve certain conflicts more efficiently than going straight to court.

Comparison Table: Regulated Brokers vs. Retail Prop Firms

| Protection Feature | Regulated Brokers | Retail Prop Firms |

|---|---|---|

| Regulatory Oversight | Supervised by SEC, CFTC, and NFA with audits | Limited oversight; operate in regulatory gray areas |

| Fund Protection | Customer protection and segregation requirements; SIPC coverage (securities broker-dealers) | Often no comparable segregation requirement; evaluation fees are at risk |

| Leverage Limits | Capped at 50:1 for major currency pairs (NFA/forex investor alert) | Often far higher, increasing risk |

| Transparency Requirements | Clear disclosure of fees and terms | Complex and sometimes unfavorable terms |

| Dispute Resolution | Formal options like NFA arbitration | Often limited contractual remedies |

| Capital Requirements | Must meet minimum net capital standards | No standardized capital requirements |

| Business Model | Executes client orders under regulatory supervision | Typically evaluation-fee-based access to “funded” programs |

One of the starkest contrasts lies in leverage. Regulated brokers are limited to a 50:1 leverage ratio for major currency pairs, helping to manage risk. Many retail programs advertise substantially higher leverage, which can amplify both gains and losses—especially during volatile market conditions.

The difference in accountability is also clear when looking at past events. For example, when regulated broker MF Global collapsed in 2011, customers had access to a court-supervised process to recover segregated funds. In contrast, unregulated retail prop firms often rely on contract terms and internal policies, which may provide fewer protections when something goes wrong.

In short, the regulatory framework governing brokers creates a level of accountability and protection that is largely absent in the prop firm space. These safeguards allow traders to better manage risk and navigate the complexities of modern trading with greater confidence.

What to Look for Before Choosing a Prop Firm

Navigating the unregulated world of prop firms requires careful research to avoid unnecessary risks. A thorough evaluation can help identify firms that operate responsibly and protect your trading capital.

Checking Reputation and Transparency

One of the best signs of a reliable firm is how long it has been in business. Firms with several years of experience tend to have stable operations and a track record of handling different market conditions. Newer firms might not have the same level of reliability or expertise.

Client feedback is another important factor. While testimonials on a firm’s website can be helpful, they might not tell the full story. For a clearer picture, check independent sources like trading forums, social media groups, and review websites. These platforms often reveal honest opinions about payout reliability, customer service, and platform performance.

When reading reviews, pay attention to patterns. Consistent complaints about delayed payments or poor customer service are major red flags. On the other hand, firms that handle payouts efficiently and resolve disputes fairly are worth considering.

Transparency is key. A trustworthy firm will clearly explain its trading conditions, risk policies, and fee structures. Look for firms that openly discuss how they operate, how they make money, and how profit-sharing works. This information should be easy to find on their website, in their documentation, or through customer service.

Even though most prop firms aren’t regulated like traditional brokers, they should still have proper business registrations or affiliations. If a firm lists registration details on its website, take the time to verify them through official channels.

Reviewing Legal Documentation and Terms of Service

A firm’s website and content can reveal a lot about its professionalism. A well-maintained site should provide clear information about risks, trading rules, and compliance measures. It should also include contact details, a physical address, and background information about the firm.

When reviewing legal documents, focus on the terms of service and user agreements. These should clearly outline your rights, the firm’s responsibilities, and how disputes are handled. If the language is overly complicated or vague, it could be a sign that the firm is trying to hide unfavorable terms.

Testing customer service is another way to gauge a firm’s reliability. Before committing any funds, ask specific questions about their fees, payout processes, and operations. A responsive and knowledgeable support team is a good indicator of a firm’s transparency.

Legitimate firms should also be willing to share their business registration certificates and audit reports. If a firm refuses to provide this information or claims it’s “proprietary,” proceed with caution.

Finally, research the firm’s complaint history. Check government databases for any violations, disciplinary actions, or legal disputes.

Checklist for Vetting Prop Firms

| Evaluation Category | Key Verification Steps | Red Flags to Avoid |

|---|---|---|

| Business Legitimacy | Verify registration and physical address; Check history (2+ years preferred) | No verifiable registration; P.O. box address; Aggressive marketing from new firms |

| Financial Transparency | Review fee schedules and profit-sharing terms; Confirm payout timelines | Hidden fees; Unclear profit-sharing terms; Vague payout processes |

| Documentation Quality | Check terms of service, audit reports, and risk disclosures | Complex legal language; Missing risk disclosures; Refusal to provide documents |

| Community Feedback | Read independent reviews; Engage with traders on forums and social media | Negative reviews; Complaints about delayed payouts; Poor customer service |

| Customer Support | Test response times; Assess staff knowledge; Check availability across time zones | Slow responses; Evasive answers; Limited contact options |

| Technology Platform | Test platform stability, demo account performance, and data feed reliability | Frequent outages; Limited features; Poor execution quality |

It’s also important to keep an eye on the firm after you’ve signed up. Join trader communities focused on your chosen firm to stay updated on any changes or issues.

Fee structure analysis is another critical step. Look at all potential costs, including evaluation fees, monthly subscriptions, profit splits, and withdrawal charges. Calculate the total cost over time to understand your financial commitment. Transparent firms will provide a clear breakdown of fees upfront.

Finally, focus on firms that prioritize trader development. The best firms invest in education, offer ongoing support, and set fair evaluation criteria that reward genuine trading skill—not just lucky outcomes. These measures can help you manage risks and succeed in an unregulated trading environment.

Future of Prop Firm Regulation in the U.S.

The regulatory environment for retail prop firms is undergoing significant changes. What was once a largely unregulated space is now moving toward closer scrutiny, enforcement, and clearer standards around marketing, risk disclosures, and consumer protections. These changes aim to create a more structured environment, giving traders clearer guidelines to navigate and adapt their strategies.

Possible Regulatory Frameworks Under Discussion

Currently, many retail prop programs operate with minimal direct oversight, but that may continue to evolve. Future regulation is likely to focus on recurring issues such as opaque evaluation criteria, unclear payout eligibility rules, and marketing claims that blur the line between simulated and live trading. Instead of outright bans, regulators often favor practical measures such as clearer disclosures, licensing requirements where applicable, capital adequacy standards for regulated entities, periodic audits, and stronger identity and compliance controls (including AML-related procedures where required).

Trends Toward Increased Oversight and Transparency

The push for stricter oversight is gaining momentum globally. For example, regulators have publicly targeted misleading or unlawful financial promotions on social media, including coordinated actions aimed at “finfluencers.” The UK’s regulator has described international crackdowns on illegal financial promotions, urging consumers to verify firms and promotions before engaging FCA release.

At the same time, firm-published data suggests that success rates can be meaningfully lower than marketing headlines imply. Some firms report that only a fraction of participants advance to funded stages within a calendar year, and only a portion of funded traders receive payouts (when firms publish such data). This is one reason due diligence should include reading firm rules, understanding how payouts work, and stress-testing your approach before paying repeated evaluation fees.

How Traders Can Prepare for Regulatory Changes

As new rules and enforcement trends emerge, traders must step up their preparation. Relying on marketing claims or testimonials won’t be enough. Instead, focus on strengthening core trading skills and building strategies that perform consistently across various market conditions. Keeping detailed records of agreements, communications, and trading performance with prop firms will also be crucial, especially as new consumer protections come into play. Staying updated on regulatory developments through official announcements will help traders adapt quickly. Finally, refining essential skills like risk management and maintaining consistent profitability will be vital for long-term success.

The move toward increased scrutiny signals a maturing industry. While it may create short-term challenges, the long-term effects should provide better protections for traders and encourage more sustainable business practices among legitimate firms.

Tools for Strategy Development

As regulatory changes continue to reshape the prop trading landscape, traders need reliable ways to craft and test strategies capable of handling volatility and shifting rules. In 2026, strategy development has moved further toward a data-driven process, combining technical analysis with systematic validation.

The Role of Technical Analysis and AI

In modern prop trading, technical analysis is essential, and AI-driven workflows can help traders evaluate ideas faster and more consistently. By processing multiple timeframes at once, identifying recurring market patterns, and providing structured feedback on performance, AI can reduce guesswork and help traders focus on repeatable decision-making.

If you want to pair discretionary analysis with structured testing, it helps to combine chart-based frameworks (like market structure and trend context) with a repeatable backtesting workflow that measures how rules behave across instruments and conditions.

LuxAlgo AI Backtesting Assistant

One standout option is LuxAlgo’s AI Backtesting Assistant, LuxAlgo’s AI agent for creating trading strategies. It supports automated, data-driven analysis and performance feedback so traders can iterate on strategies while keeping risk constraints in focus.

LuxAlgo also provides three exclusive toolkits on TradingView—Price Action Concepts, Signals & Overlays, and Oscillator Matrix—along with TradingView screeners and backtesters that help traders filter opportunities and validate rule-sets more efficiently. For example, traders can scan across symbols using the PAC Screener, S&O Screener, and OSC Screener.

Once you’ve identified a concept you want to validate, LuxAlgo’s TradingView backtesters can help you systematically test entry/exit logic: Backtester (PAC), Backtester (S&O), and Backtester (OSC). This is particularly useful for prop firm environments where drawdown rules and daily loss limits punish inconsistency.

Plans & Pricing

- Free Plan: $0, lifetime access. Includes hundreds of tools across 5+ platforms.

- Premium: $39.99/month – advanced signals, alerts, and oscillator tools on TradingView.

- Ultimate: $59.99/month – includes AI Backtesting platform.

To compare plans, see LuxAlgo pricing. To get started quickly, explore the AI Backtesting documentation for workflow examples and strategy ideas.

Regular Strategy Testing for Long-Term Success

In today’s fast-changing market, continuous strategy testing and refinement are essential. The most successful traders understand that strategy development isn’t a one-and-done task; it’s an ongoing process.

Regular testing allows traders to identify and address weaknesses before they lead to costly mistakes. This is particularly critical in prop trading, where firms often enforce strict rules around maximum drawdowns and daily loss limits. A strategy that works well in trending markets may fail during periods of high volatility or sideways movement.

To stay ahead, adopt a systematic approach to evaluation: set clear objectives and risk parameters, use reliable technical analysis and AI workflows, test strategies on relevant historical samples, and regularly review performance metrics. Monitor changes in market conditions and firm rules, while documenting adjustments and results for future reference. If you’re building your process around LuxAlgo workflows, it can help to start with the AI Backtesting Assistant introduction and map your rule-set into a backtester that matches your style.

Conclusion: Key Takeaways for Traders

Reflecting on the risks, protections, and due diligence strategies we’ve discussed, here are key points for traders to keep in mind. The retail prop trading industry in the United States offers opportunities for growth but comes with challenges. While these firms provide access to capital and a chance to earn, the lack of robust regulatory oversight leaves traders vulnerable to risks that could jeopardize progress.

Understanding Risks and Protections

Regulated brokers come with safeguards like SIPC coverage (in applicable cases), customer protection requirements, and structured dispute resolution processes. Unregulated prop firms often lack comparable protections, leaving traders exposed to potential losses, including their profits and evaluation fees. A major concern is the misleading marketing language some firms use, implying protections similar to brokers while operating under entirely different legal frameworks.

Steps to Evaluate Prop Firms

To navigate this landscape, thorough research is crucial. Start by verifying the firm’s legal registration and carefully reviewing its payout rules and contract terms. A firm with a documented track record of payouts over several years can be a positive sign, but it’s still essential to understand the exact eligibility criteria and the firm’s discretion under its policies.

Also, consider the firm’s business model. Firms that rely heavily on evaluation fees rather than trader performance may have misaligned incentives. Look for companies that invest in trader development through education, structured rule-sets, and transparent performance frameworks. Beyond vetting firms, traders can build a stronger edge by adopting repeatable testing workflows before paying multiple evaluations.

Leveraging Technology for Smarter Trading

Adopting data-driven strategies can help traders succeed in any regulatory environment. LuxAlgo AI Backtesting enables traders to test and refine strategies across market conditions before risking capital—particularly useful when working with prop firms that impose strict drawdown limits and performance benchmarks.

The biggest advantage of strong, well-tested strategies is their ability to deliver results regardless of the regulatory framework. Whether you’re trading with a regulated broker, a carefully vetted prop firm, or your own capital, having a solid strategy gives you the flexibility and control needed to navigate your trading career effectively.

As regulations evolve, the combination of careful firm evaluation, regulatory awareness, and advanced trading workflows lays a strong foundation for long-term success in trading.

FAQs

How can traders choose a trustworthy retail prop firm when regulations are limited?

When choosing a dependable retail prop firm, it’s essential to focus on clarity and trustworthiness. Start by examining their website—does it look professional and provide detailed information about their operations and history? A firm with a documented track record of timely payouts and clear eligibility rules is generally safer than one that relies on vague promises.

Take time to read independent reviews on reputable platforms. Pay attention to feedback from other traders and lean toward firms that consistently receive positive ratings, particularly regarding payout processing and customer support.

It’s also worth checking whether the firm is registered or connected to any official organizations. While many operate in lightly supervised environments, those that are upfront about their practices and maintain a strong reputation are generally safer choices. Always conduct thorough research to ensure your time and fees aren’t being wasted.

How could future regulations affect retail prop firms and traders who use them?

Future regulations may tighten oversight and introduce clearer compliance expectations for retail prop firms—especially around marketing claims, transparency of rules, and disclosure of simulated vs. live trading conditions. While this could increase costs for firms, it may also encourage clearer business practices and improve trader protections.

On the flip side, stricter requirements could reduce the flexibility of some firms, potentially forcing them to modify programs or exit certain markets. For traders, this might mean new onboarding steps, more disclosures, and stricter enforcement of rules, which could affect access to funded accounts and alter the overall trading experience.

What are the best ways for traders to reduce risks when working with unregulated prop firms?

When trading with unregulated prop firms, taking steps to protect yourself is essential. Start with thorough research. Investigate the firm’s reputation, rule enforcement style, payout history, and level of transparency before committing any funds. Look for consistent, verifiable information rather than hype.

Next, focus on risk management. Tools like stop-loss and take-profit and stop-loss placement rules can help limit downside, while avoiding over-leveraging can reduce the chance a single mistake ends your account. Diversifying your trading approaches and not relying on one firm also lowers the risk of being caught off guard by sudden rule changes or payout delays.

Lastly, take a cautious approach. Track changes to terms, screenshot key rules, and avoid repeatedly paying evaluations without a measured plan. By spreading your risk and staying alert, you can better protect yourself in an unpredictable environment.

References

LuxAlgo Resources

- Traditional Proprietary Trading: An Insider’s Guide

- Trading Strategies (Topic)

- AI Backtesting Documentation (Intro)

- LuxAlgo – Official Site

- AI Backtesting Assistant

- LuxAlgo Prop Firms & Trading Strategies Hub

- Price Action Concepts Toolkit (Intro)

- Signals & Overlays Toolkit (Intro)

- Oscillator Matrix Toolkit (Intro)

- PAC Screener (Intro)

- S&O Screener (Intro)

- OSC Screener (Intro)

- Backtester (PAC) (Intro)

- Backtester (S&O) (Intro)

- Backtester (OSC) (Intro)

- LuxAlgo Pricing

External Resources

- U.S. Securities and Exchange Commission (SEC)

- Commodity Futures Trading Commission (CFTC)

- National Futures Association (NFA)

- Securities Investor Protection Corporation (SIPC)

- FINRA: Segregation of Assets & Customer Protection (SEA Rule 15c3-3)

- SEC: AML Source Tool for Broker-Dealers

- Blue Sky Laws Overview (Investopedia)

- NASAA: Uniform Securities Acts & State Securities Laws

- NFA: Forex Investor Alert & Leverage

- NFA Arbitration Program

- Topstep: Published Trader Performance Statistics

- ASIC: Global Action Against Unlawful Finfluencers

- FCA: International Crackdown on Illegal Finfluencers

- MF Global (Background)